How to Read Your Construction Financial Statements — What Each Number Actually Means

- Cost Construction Accounting

- May 8

- 8 min read

By Tammy Hoang, QuickBooks ProAdvisor | Construction Cost Accounting | calendly.com/tammycca/30min

Every month, construction business owners receive a set of financial statements from their bookkeeper or accountant. Most of them look at two numbers — revenue and net income — and move on. The rest of the report sits unread. This is one of the most expensive habits in construction accounting, because the numbers that actually tell you whether your business is healthy are not the ones at the top and bottom of the page. Construction financial statements are different from those of a retail store or a law firm. They include project-specific data — job cost reports, WIP schedules, retainage balances, overbilling and underbilling positions — that a standard income statement and balance sheet do not capture. When a construction bookkeeping services provider gives you your monthly financials, they are handing you a dashboard of your business. Knowing how to read that dashboard is the difference between making decisions based on real information and running your company on gut feel. This post is a plain-language guide to what each statement shows, what numbers to look at first, and what red flags to watch for — written from the perspective of a QuickBooks ProAdvisor with over fifteen years of bookkeeping for contractors in Orange County and across California.

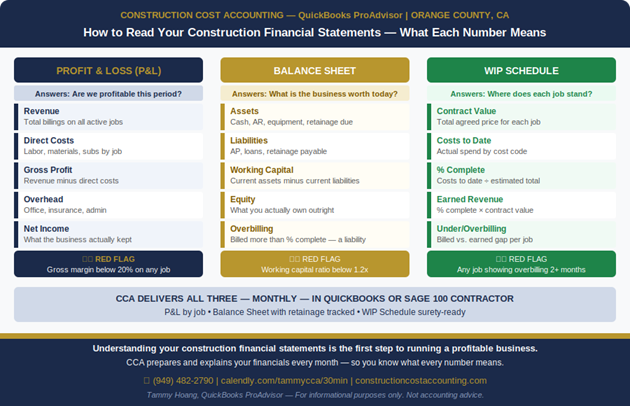

The Profit and Loss Statement — What It Shows and What It Misses

The profit and loss statement — also called the P&L or income statement — is the financial statement most contractors look at first. It shows your total revenue for the period, your direct costs, your gross profit, your overhead expenses, and your net income. In standard accounting for construction companies, revenue on the P&L is recognized using either the percentage of completion method or the completed contract method, depending on how your construction accounting is structured in QuickBooks Online construction or Sage 100 Contractor. What the P&L shows: whether your business was profitable during the period. What the P&L misses: which specific jobs were profitable, which ones lost money, and whether the revenue recognized matches the actual work completed on each project. This is the core limitation of reading only the P&L in a construction business. A contractor can show strong net income on the P&L while three of their active jobs are losing money — because job-level profitability is buried in the job cost reports, not visible in the summary P&L. The numbers to look at first on your P&L are gross margin percentage by job, not just overall, and the relationship between your overhead and your revenue. If your overhead is growing faster than your revenue, that shows up in the net income

line — but only after the damage is done. Construction bookkeeping services that produce monthly job-cost-level P&L breakdowns give you a much more accurate picture than a single consolidated income statement. When your bookkeeping for contractors is set up correctly in QuickBooks Online construction, you can pull a P&L by customer or job and see exactly which projects are carrying the business and which ones are bleeding it.

The Balance Sheet — What Your Construction Business Is Worth Right Now

The balance sheet is a snapshot of your business's financial position on a single date. It shows what you own (assets), what you owe (liabilities), and what is left over (equity). For construction accounting, the balance sheet has several line items that require construction-specific bookkeeping to track correctly — and that most general bookkeepers get wrong. Assets on a construction balance sheet include cash, accounts receivable, retainage receivable (money earned but withheld by the GC or owner), equipment, and underbilling — which represents work completed that has not yet been billed. Liabilities include accounts payable, loans, retainage payable (amounts you are withholding from your subcontractors), and overbilling — which represents amounts billed in excess of the work actually completed. Overbilling is the one that surprises most contractors. In accounting for construction companies, overbilling is a liability — not income. You billed for it, but you have not earned it yet because the work is not far enough along. Surety companies review your balance sheet to evaluate bonding capacity, and an overbilling position that looks like a pattern is a red flag to any surety underwriter. The number to watch first on your balance sheet is working capital — current assets minus current liabilities. For a healthy construction business, this ratio should be above 1.2x. If it drops below 1.0x, your business cannot comfortably meet its short-term obligations, which creates contractor cash flow risk even if your P&L looks profitable. Construction bookkeeping that tracks retainage receivable and payable separately, codes overbilling and underbilling correctly, and reconciles the balance sheet monthly is what makes this number reliable. In QuickBooks Online construction, this requires a properly structured chart of accounts and job coding — which is one of the first things CCA sets up for every new client.

Construction Financial Statement Red Flags — What CCA Watches Every Month

The table below shows the specific numbers CCA monitors in every client's construction financial statements each month — and what each red flag signals before it becomes a real problem. This is the practical value of construction bookkeeping services that go beyond data entry and actually review what the numbers are saying.

Statement | Red Flag Number | What It Signals |

P&L — Gross Margin | Below 20% on any job | Labor or material cost overrun — underbid or untracked cost |

P&L — Net Income | Negative despite revenue | Overhead too high or jobs not profitable after all costs |

Balance Sheet — Working Capital | Ratio below 1.2x | Business cannot comfortably cover short-term obligations |

Balance Sheet — Overbilling | Overbilling exceeds 10% of revenue | Revenue recognized faster than work completed — surety risk |

WIP Schedule — Underbilling | 2+ months of underbilling on same job | Cash flow gap — work done but not yet billed |

WIP Schedule — Loss Job | Estimated cost exceeds contract | Book the full loss immediately — GAAP requirement |

Cash Flow Statement — Operating | Negative cash from operations | Profitable on paper but running out of actual cash |

None of these red flags are visible if you only look at the summary P&L once a month. They require construction-specific bookkeeping that produces the WIP schedule, tracks retainage separately, codes overbilling and underbilling correctly, and reconciles every account to the bank statement. This is standard in CCA's monthly construction bookkeeping services — and it is what separates bookkeeping for contractors from general business bookkeeping.

The WIP Schedule — The Construction Financial Statement Your CPA Does Not Produce

The WIP schedule — Work in Progress schedule — is the construction financial statement that most business bookkeeping does not produce at all, and the one that construction accounting for construction companies relies on most heavily. It is not generated automatically by QuickBooks Online construction or any standard accounting software. It requires a bookkeeper who understands construction financials at a job level and knows how to calculate percentage of completion, earned revenue, and the underbilling or overbilling position for every active project. Here is what the WIP schedule shows. For each active job: the total contract value, the total costs incurred to date, the percentage complete based on costs, the revenue earned to date based on that percentage, the amount actually billed to date, and the difference between billed and earned — which is either overbilling (billed more than earned — a liability) or underbilling (earned more than billed — an asset that has not been invoiced yet). The WIP schedule is what your surety uses to evaluate bonding capacity. It is what your lender reviews to evaluate your line of credit. It is what your construction CPA needs to advise correctly on your revenue recognition method. And it is what your construction bookkeeping services provider should be producing every single month — not just at year-end. At CCA, the WIP schedule is part of the standard monthly package for every client. We build it in QuickBooks Online construction or Sage 100 Contractor, reconcile it to the job cost reports, and flag any job showing overbilling, underbilling, or an anticipated loss — before those numbers reach your CPA or your surety.

Your Construction Financial Statements Should Tell You What to Do Next

If your monthly construction financials are a stack of reports you do not know how to read — or if your current bookkeeper produces a P&L and balance sheet but no WIP schedule — your construction bookkeeping is not giving you what you need to run the business. Construction Cost Accounting provides construction bookkeeping services for contractors throughout Orange County and across California. Every month we deliver a full package of construction financial statements — P&L by job, balance sheet with retainage tracked correctly, WIP schedule surety-ready, and a cash flow statement — built in QuickBooks Online construction or Sage 100 Contractor. We go through the numbers with you. We flag the red flags before they become problems. We give you the financial clarity that lets you bid confidently, manage cash, and make real decisions. If you want construction financials that actually tell you something — book a free 30-minute consultation with Tammy. Call (949) 482-2790 or schedule directly below.

Frequently Asked Questions — Construction Financial Statements

What financial statements does a construction company need?

A construction company needs four core financial statements: a profit and loss statement (P&L), a balance sheet, a cash flow statement, and a WIP schedule. Standard accounting for construction companies requires all four — not just a P&L. The WIP schedule is the most construction-specific and is not produced by general bookkeeping software automatically. CCA delivers all four as part of the monthly construction bookkeeping services package for every client.

What is a WIP schedule in construction accounting?

A WIP schedule — Work in Progress schedule — is a construction financial statement that shows where every active job stands financially. It calculates the percentage of completion for each project, the revenue earned based on that percentage, and the overbilling or underbilling position. Surety companies, lenders, and construction CPAs all rely on the WIP schedule. CCA produces it monthly in QuickBooks Online construction or Sage 100 Contractor for every client.

What should a contractor look for in their P&L?

In your construction P&L, look at gross margin percentage by job — not just the overall total. A healthy construction business typically targets 20–30% gross margin per project. If any job is below 15%, that is a flag worth investigating with your bookkeeper for contractors. Also watch the relationship between overhead and revenue — overhead growing faster than revenue is a warning sign that net income will compress even if jobs appear profitable.

What does overbilling mean on a construction balance sheet?

Overbilling on a construction balance sheet means your company has billed more than the percentage of work actually completed on a project. In accounting for construction companies, overbilling is recorded as a liability — not income — because you owe the corresponding work. Surety companies flag overbilling patterns when reviewing bonding capacity. CCA tracks overbilling and underbilling monthly through the WIP schedule and flags any job that shows a concerning position.

Does CCA provide monthly construction financial statements in Orange County?

Yes. Construction Cost Accounting provides complete monthly construction financial statements for contractors throughout Orange County and California. Our construction bookkeeping services include a monthly P&L by job, balance sheet with retainage tracked separately, WIP schedule, cash flow statement, and red flag review — all built in QuickBooks Online construction or Sage 100 Contractor. Call (949) 482-2790 or book at calendly.com/tammycca/30min.

Comments