Loss Contracts in Construction — What GAAP Requires and How CCA Catches Them Before Your CPA Does

- Cost Construction Accounting

- May 6

- 8 min read

By Tammy Hoang, QuickBooks ProAdvisor | Construction Cost Accounting | calendly.com/tammycca/30min

Most construction contractors know what a loss looks like when it shows up at year-end — a job that ran over budget, margins that disappeared, a number their CPA presents in April that nobody saw coming. What most contractors do not know is that under GAAP, that loss should have been on the books the moment it became evident — not months later when the damage was done. This is the problem of the loss contract in construction accounting: a project where total estimated costs exceed total contract revenue, and a very specific accounting requirement that contractors and their bookkeepers frequently miss. As a QuickBooks ProAdvisor specializing in construction bookkeeping in Orange County, I review WIP schedules monthly for exactly this reason. Loss contract construction situations are one of the most common — and most expensive — accounting mistakes that construction companies make. This post explains what the GAAP rule requires, why contractors miss it, and how CCA's monthly job costing process catches it before your CPA does.

What Is a Loss Contract in Construction?

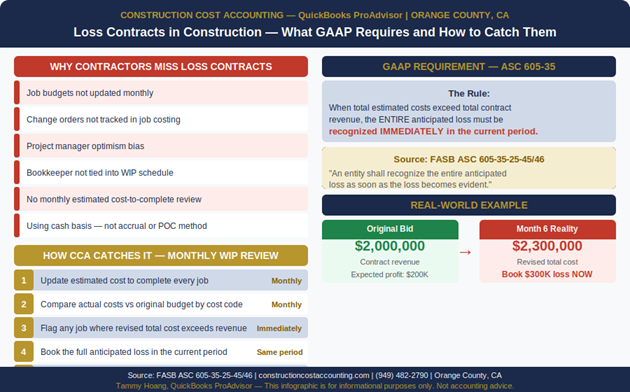

A loss contract in construction is any project where the current estimate of total costs to complete exceeds the total consideration — the contract revenue — the contractor expects to receive. This is not the same as a job that had a bad month. It is a job where the entire project, from mobilization through completion, is now projected to finish in the red. Under GAAP — specifically FASB ASC 605-35-25-45 — when a contractor using the percentage of completion method determines that a contract will result in a net loss, the entire anticipated loss must be recognized immediately in the period it becomes evident. Not spread over the remaining months of work. Not deferred to the period of completion. The full loss hits the income statement the moment the updated estimate shows a loss. The rule exists because percentage of completion accounting continuously recognizes revenue and profit as work progresses. Without the loss contract rule, a contractor could report positive margins in month four on a job that is headed for a $300,000 loss at completion — misleading lenders, sureties, and owners about the true financial position of the company. A loss contract in construction is a compliance requirement, not just a bad day on the job site.

What GAAP Requires — ASC 605-35 Decision Table

The table below shows how ASC 605-35 applies depending on where your revised cost estimate lands. Source: FASB ASC 605-35-25-45/46.

Scenario | GAAP Treatment — ASC 605-35 |

Revised cost estimate still shows profit | No change — continue recognizing profit using percentage of completion method as normal |

Revised cost estimate shows break-even | No loss provision required — monitor closely each period |

Revised cost estimate shows a loss | Book the ENTIRE anticipated loss immediately in the current period — not spread over remaining months |

Loss grows larger in a later period | Recognize additional loss immediately when identified — do not defer |

Project scope changes and loss reverses | Reverse the loss provision in the period the change is confirmed and documented |

Why Construction Contractors Miss Loss Contracts — 6 Root Causes

In over fifteen years of construction bookkeeping in Orange County and across California, the same six root causes come up again and again when a contractor misses a loss contract until it is too late. The first is job budgets that are not updated monthly. If your original bid budget sits unchanged from month one through month ten, you have no mechanism to know when cost overruns have pushed a job into loss territory. The second is change orders that are tracked on the project management side but never flow into the job costing system. A contractor might have $80,000 in approved change orders that reduced the scope — meaning total revenue dropped — but the cost estimate was never adjusted to match. The third is what I call project manager optimism bias. PMs are paid to deliver projects. They are not paid to report losses to ownership. The natural tendency is to assume the overrun will be recovered in the next phase. It usually is not. The fourth is a bookkeeper who is not tied into the WIP schedule — meaning construction cost overrun accounting gets discovered at year-end rather than month by month. If the person entering transactions in QuickBooks is not also reviewing estimated cost to complete each month, the job costing data and the accounting data tell different stories. The fifth is using cash basis accounting, which does not recognize revenue or cost until cash changes hands — making the percentage of completion method and its loss contract rules inapplicable, but also making it impossible to know where any individual job stands financially until it is over. The sixth is simply not knowing the rule exists. Many contractors and even some general-purpose bookkeepers have never heard of ASC 605-35 — it is one of the construction accounting mistakes most often discovered only when a CPA flags it at year-end. They know what a bad job looks like. They do not know they were required to book the loss the month they figured it out.

The Real Cost of Missing a Loss Contract — A Contractor Example

Consider a general contractor in Orange County who bids a $2,000,000 commercial renovation. Original cost estimate: $1,800,000. Expected profit: $200,000 at 10% margin. By month six, material costs have spiked due to tariffs and supply chain delays. A subcontractor has gone over on their scope and submitted a change order the GC is disputing. The updated cost estimate is now $2,300,000. The job is projected to lose $300,000. Under ASC 605-35, the entire $300,000 anticipated loss must be booked in month six — the period in which the loss became evident. If the bookkeeper does not run an updated WIP schedule in month six, the company's financial statements will show positive margins from the percentage of completion revenue recognized to date. The surety reviewing the company's interim financials for a bonding renewal will see a profitable company. The lender reviewing financials for a line of credit draw will see a profitable company. The owner reviewing the monthly P&L will see a profitable company. None of these are true. The loss is real. It is just not on the books yet. When it finally shows up — at year-end, when the CPA prepares the audited or reviewed statements — it hits all at once. A $300,000 surprise. Bonding capacity drops. Credit review is triggered. Cash flow planning was built on numbers that were wrong for six months. This is the cost of missing a construction contract loss recognition. It is not an accounting technicality. It is a business risk.

How CCA Catches Loss Contracts — The Monthly WIP Process

At Construction Cost Accounting, catching loss contracts before the CPA does is part of the monthly bookkeeping workflow — not a special audit. Here is how it works. Every month, after transactions are posted and reconciled in QuickBooks or Sage 100 Contractor, we run an updated WIP schedule for every active job. The WIP schedule compares three numbers for each project: the original contract value, the actual costs incurred to date, and the revised estimated cost to complete. When estimated cost to complete plus costs incurred to date exceeds the contract value, that job is flagged. We calculate the anticipated loss at the contract level — consistent with ASC 605-35 requirements — and bring it to the owner's attention immediately, not at year-end. The owner then has three options: adjust the scope through a legitimate change order, find cost savings in the remaining work that would restore the margin, or book the loss provision now and manage cash flow accordingly. None of these options are available if the problem is discovered in April by a CPA preparing year-end statements. The percentage of completion loss recognition requirement under GAAP is not a technicality for large public companies. It applies to any construction contractor using the percentage of completion method — which includes most contractors with jobs over $1 million or multi-year projects. If your current construction bookkeeping in Orange County or anywhere in California is not running monthly WIP schedules, you are not catching loss contracts in construction on time.

Does Your Bookkeeper Run a Monthly WIP Schedule?

If the answer is no — or if you are not sure — there is a real probability that loss contracts in your portfolio are going unrecognized until your CPA finds them. Failure to recognize an anticipated loss on construction contract work is one of the most common and costly construction accounting mistakes that contractors in Orange County make. The construction cost overrun accounting problem compounds every month that the WIP schedule construction accounting review does not happen — because each month of percentage of completion loss going unrecognized is another month of financial statements that misrepresent the company's true position. Construction Cost Accounting provides outsourced construction bookkeeping for contractors throughout Orange County and across California. We run monthly WIP schedules, maintain construction job costing loss identification by cost code, flag construction contract loss recognition issues as soon as they become evident, and report to ownership before any surprises reach the CPA. Our outsourced construction bookkeeping service is built specifically for contractors who need more than a general bookkeeper — they need someone who understands the percentage of completion loss rules, the WIP schedule construction accounting workflow, and the construction bookkeeping Orange County market. If you want a bookkeeper who catches loss contract construction situations in month six — not month twelve — book a free 30-minute consultation with Tammy. Call (949) 482-2790 or schedule below.

Frequently Asked Questions — Loss Contracts in Construction

What is a loss contract in construction accounting?

A loss contract in construction is any project where the current estimate of total costs to complete exceeds the total contract revenue. Under GAAP — specifically FASB ASC 605-35-25-45 — the anticipated loss on construction contract work must be recognized immediately in the period it becomes evident, not deferred to project completion. Loss contract construction situations are one of the most common construction accounting mistakes that contractors miss because they are not running updated WIP schedules monthly.

What does GAAP require for loss contract recognition?

GAAP requires that when a construction contractor using the percentage of completion method determines that a project will result in a net loss, the full anticipated loss on construction contract must be booked in the current accounting period. Construction contract loss recognition applies at the contract level and cannot be spread over the remaining months of work. This percentage of completion loss rule is found in FASB ASC 605-35-25-45/46

Why do construction contractors miss loss contracts?

The most common reasons include: job budgets not updated monthly, change orders not tracked in job costing, construction cost overrun accounting that is done at year-end instead of monthly, a bookkeeper not running WIP schedule construction accounting reviews, using cash basis instead of percentage of completion, and not knowing the GAAP rule exists. Each of these is a construction accounting mistake that leads to construction contract loss recognition being delayed.

What is a WIP schedule and how does it catch loss contracts?

A WIP schedule — Work in Progress schedule — compares each job's contract value, costs incurred to date, and estimated cost to complete. WIP schedule construction accounting is the primary tool for identifying construction job costing loss situations. When estimated cost to complete plus costs to date exceeds the contract value, the job flags as an anticipated loss on construction contract work. Running this monthly as part of construction bookkeeping Orange County contractors rely on is the only way to catch the problem in time.

Does CCA provide monthly WIP schedules for construction contractors?

Yes. Construction Cost Accounting provides outsourced construction bookkeeping for contractors throughout Orange County and California. Our outsourced construction bookkeeping service includes monthly WIP schedule construction accounting reviews, construction job costing loss identification, construction bookkeeping Orange County market expertise, and construction contract loss recognition reporting to ownership before year-end. Call (949) 482-2790 or book at calendly.com/tammycca/30min.

Comments