Construction Accounting in 2026: The Complete Guide for Contractors — ASC 606, Chart of Accounts, and the Financial Reporting Every Firm Needs

- Cost Construction Accounting

- Jun 8

- 15 min read

By Tammy Hoang, QuickBooks ProAdvisor — Construction Bookkeeping Specialist | Construction Cost Accounting

(949) 889-3283 | constructioncostaccounting.com

Construction is one of the few industries where the difference between a profitable year and a losing one comes down to the books. Not the bidding, not the field execution, not the customer relationships — the books. A contractor with strong field operations but weak construction accounting routinely underbids jobs, misses cost overruns until they are unrecoverable, and finds out at year-end that the year they thought they made $400K actually made $90K. A contractor with disciplined accounting catches the same problems in week three of the job, not month nine.

This guide is built for construction firm owners and finance leads who want to understand accounting for contractors the way the industry actually practices it in 2026. We cover ASC 606 revenue recognition (the standard that determines how your revenue hits your books), construction chart of accounts structure (the foundation everything else builds on), the major revenue recognition methods, billing approaches, retainage handling, and the modern accounting software landscape — what fits a $2M residential remodeler, what fits a $20M commercial GC, and what fits everything in between.

Construction Cost Accounting is a construction-specialized construction bookkeeper and QuickBooks ProAdvisor firm serving Orange County contractors. As a marketing agency near me for construction financial clarity, we configure books, build chart of accounts structures, run monthly close, and produce the financial reports surety companies and CPAs expect from contractors. This guide reflects what we see in active engagements every month.

What Is Construction Accounting?

Construction accounting is a specialized branch of accounting built around the way construction projects actually work — long timelines, mobile labor, project-by-project profitability, customized scope, and unique billing arrangements that do not exist in retail, manufacturing, or service businesses. Where regular accounting tracks income and expense at the company level, construction accounting tracks them at the project level — each job is its own profit center, and each job is accounted for separately.

The core difference: regular businesses know if they are profitable when month-end income exceeds month-end expense. Construction businesses do not. A construction firm can run six profitable months while quietly losing money on the three large jobs that will not finish until next year. The only way to know is to track each project independently — which is what construction accounting exists to do.

Per the Construction Financial Management Association (CFMA), disciplined accounting for construction companies is what separates contractors who scale sustainably from those who grow into financial trouble. The math is simple: more revenue without better accounting just means bigger losses hidden longer.

Construction Accounting Basics: Why Construction Is Different

Before getting into the methods and frameworks, the foundation of construction accounting basics is understanding what makes construction structurally different from every other industry:

Long contract cycles — projects run months to years, with cash flowing in lumps rather than steadily. A $2M project might generate one payment in week 4 and the next in week 12. Revenue and cash do not match up cleanly.

Project-by-project profitability — total company profit means little. Each job has its own gross margin, its own cost code structure, its own variances. Profitable companies can have unprofitable jobs hiding inside them — and vice versa.

Mobile, customized labor — crews move between job sites, often across multiple jobs in one week. Labor costs have to be allocated to specific projects, not just dumped into a single payroll expense line.

Multiple cost categories — direct labor, indirect labor, materials, equipment rental, subcontractor commitments, mobilization, permits, bonds, insurance. Each lives in its own line and ties to its own project.

Variable consideration — change orders, claims, incentives, and disputed amounts that can shift the contract price after signing. Standard businesses do not deal with this.

Retainage — 5–10% of every progress payment withheld until substantial completion. Earned revenue you cannot collect until the project is done.

The single biggest mistake regular bookkeepers make on construction clients is treating each invoice the way they would in any other industry — without project allocation. Within a quarter, the books are unreadable. |

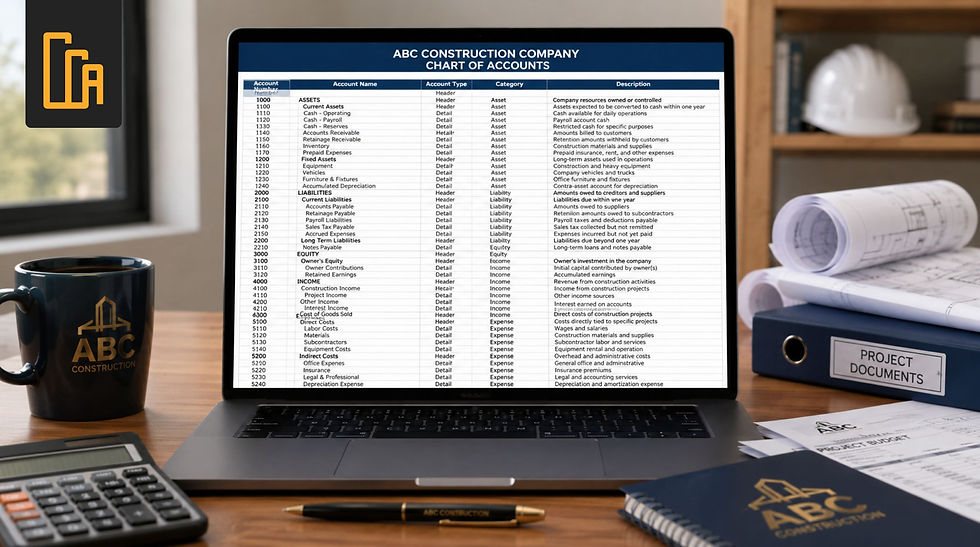

Construction Company Chart of Accounts.

The construction company chart of accounts is the structural foundation of your entire accounting system. Get it right and every report — P&L, balance sheet, WIP, job cost — comes out clean. Get it wrong and every report misses something. A construction chart of accounts looks very different from a generic small-business chart because it is built around the structure of how construction actually operates.

The Five Layers of a Construction Chart of Accounts

Assets — cash accounts, accounts receivable (with retention separated as its own subaccount), work-in-progress, fixed assets with depreciation schedules, prepaid expenses (bonds, insurance, software).

Liabilities — accounts payable (with retention payable separated), accrued payroll, lines of credit, notes payable, deferred revenue / customer deposits, retention payable to subs.

Equity — owner's equity, retained earnings, contributions, distributions.

Revenue — contract revenue (by contract type — fixed price, T&M, cost-plus), retention earned, other income. Each revenue line should support job-level tracking.

Cost of Goods Sold (COGS) and Expenses — direct labor, indirect labor, materials, subcontractor costs, equipment, mobilization, permits, bonds, project-specific insurance, then general overhead separated as a distinct expense category below COGS.

CCA PRO TIP: The single biggest chart of accounts mistake on QuickBooks construction setups: putting overhead and direct costs in the same expense bucket. Once that happens, you cannot calculate true job profitability. CCA rebuilds construction chart of accounts as part of new client onboarding so the structure supports proper job costing from day one. |

Sample Top-Level Structure

A typical mid-size general contractor's construction company chart of accounts runs 80–150 accounts across these five layers. Specialty contractors may run leaner — 60–100 accounts. The structure typically follows this top-level pattern:

1000s — Asset accounts (cash, AR, retention receivable, WIP, fixed assets)

2000s — Liability accounts (AP, retention payable, lines of credit, accrued expenses)

3000s — Equity accounts (owner equity, retained earnings)

4000s — Revenue accounts (by contract type and project)

5000s — Direct costs / COGS (labor, materials, subs, equipment)

6000s+ — Overhead expenses (general & administrative)

ASC 606: The 5-Step Revenue Recognition Model

Revenue recognition is the most important — and most misunderstood — concept in construction accounting. Since the Financial Accounting Standards Board (FASB) implemented Accounting Standards Codification 606 in 2018, all GAAP-reporting construction companies must follow a specific five-step model. Most contractors have heard of ASC 606 construction but few firms have actually structured their books around it.

THE 5-STEP ASC 606 REVENUE RECOGNITION MODEL

The standard for recognizing revenue under GAAP — and the framework your CPA and surety expect to see

1 | Identify the Contract | Confirm a valid, enforceable agreement exists — written, oral, or implied — with agreed-upon terms and commercial substance. |

↓

2 | Identify Performance Obligations | Break the contract into the distinct goods or services you've promised. One job can have one obligation — or many. |

↓

3 | Determine the Transaction Price | Calculate the total expected consideration — base contract plus variable consideration (change orders, incentives, claims) with constraint analysis. |

↓

4 | Allocate Price to Obligations | Spread the transaction price across each performance obligation based on standalone selling price. |

↓

5 | Recognize Revenue | Recognize revenue as (or when) each performance obligation is satisfied — usually over time for construction, using cost-to-cost. |

Source: FASB ASC 606 / Construction Cost Accounting | constructioncostaccounting.com

How This Plays Out in Practice

For most construction contracts, revenue is recognized over time — not at completion — because at least one of three criteria is met: the customer simultaneously receives and consumes the benefits as work progresses, the customer controls the asset as it is created (typical when building on customer-owned land), or the contractor is creating an asset with no alternative use and has an enforceable right to payment for work completed to date.

This is why the construction revenue recognition approach known as percentage-of-completion (PCM) — specifically the cost-to-cost variant — remains the dominant method under ASC 606. You divide costs incurred to date by total estimated costs to determine the percentage complete, then recognize that percentage of the contract revenue.

⚠ WATCH OUT: Unapproved change orders are one of the most common ASC 606 trip-wires. Recognizing revenue from a change order that has not been formally approved — without proper constraint analysis on variable consideration — can lead to revenue being overstated and EBITDA being inflated. CCA's monthly close process flags unapproved variable consideration for review before it hits the books. |

Construction Accounting vs Regular Accounting

The differences between construction accounting and regular accounting matter more than they appear. The four key contrasts:

Sales

Regular business: 1–5 product or service categories. Revenue is straightforward to categorize.

Construction: Wider scope — consulting, engineering, labor, materials, subcontractor management, equipment rental, often blended in a single contract. Revenue categorization requires more thought.

Cost of Goods Sold

Regular business: Simple — record the cost of products sold.

Construction: Hundreds of cost categories per project. Direct labor by trade, indirect labor, materials by type, subcontractor commitments, equipment rental, mobilization. Each tied to a specific job.

Expenses / Overhead

Regular business: Clear distinction between COGS and overhead. A retail business knows which costs are tied to products and which are administrative.

Construction: The lines blur. Project superintendents are direct cost; office administrators are overhead. Equipment rental is direct; equipment depreciation is overhead. Allocation rules have to be defined and applied consistently.

Break-Even Analysis

Regular business: Income and expenses are directly related; break-even is calculable at the product level.

Construction: Break-even has to be calculated per project, factoring in indirect cost allocation, equipment cost recovery, and overhead absorption. The same firm can be profitable on small jobs and unprofitable on large ones — or vice versa.

Common Cost Types in Construction Accounting

Job Costing

Job costing is the discipline of tracking every cost — labor, materials, subs, equipment, overhead allocation — to a specific project. It is the most important practice in construction accounting principles, because without it you cannot tell which jobs are making money and which are losing it. Most construction project management software (JobTread, Procore, Buildertrend) now syncs job costing data directly into QuickBooks for real-time visibility.

Work In Progress (WIP)

Work in progress refers to ongoing projects that are partially complete. WIP reports — produced monthly — track for each active project: contract value, costs incurred to date, percent complete, earned revenue, billed to date, and over/under billing. WIP is what tells a contractor and their CPA whether the books accurately reflect the status of every active job.

Cost of Goods Sold (COGS)

In construction, COGS includes direct costs associated with completing each project — direct labor, materials, subcontractor costs, equipment, and any other costs directly attributable to specific jobs. Analyzing COGS by project is essential to calculating true gross margin job-by-job and identifying which work types or customer segments are most profitable.

Variable Consideration

This is the ASC 606 term for amounts that may change after the original contract — change orders, claims, retainage, incentives, penalties. Under ASC 606, contractors must apply constraint analysis: only include variable consideration in the transaction price if it is highly probable that a significant reversal will not occur. Most contractors handle this wrong by either recognizing too aggressively or too conservatively. Both create financial reporting problems.

BOOKKEEPER'S NOTE: Variable consideration is where construction accounting most often goes off the rails — especially around change orders. Recognizing unapproved change order revenue inflates the books; ignoring approved change order revenue understates them. The correct treatment requires monthly review of every active job. CCA handles this as part of standard construction bookkeeping services. |

Revenue Recognition Methods Explained

Percentage of Completion (Cost-to-Cost Method)

Under ASC 606, the dominant method for construction revenue recognition on long-term contracts. Calculate the percentage complete by dividing costs incurred to date by total estimated costs. Recognize that percentage of contract revenue.

Example: A $500,000 fixed-price contract with $300,000 in estimated total costs. As of month-end, you have incurred $90,000 in costs. Percentage complete is 30% ($90,000 ÷ $300,000). Revenue recognized: $150,000 (30% of $500,000). Gross profit recognized: $60,000 ($150,000 − $90,000).

Output Methods

ASC 606 also permits output-based measurement — milestones reached, units produced or delivered, surveys of value transferred. Used when output can be measured directly and is a faithful depiction of performance. Common on production contracts (homes built, units installed) rather than custom construction.

Completed Contract Method (CCM)

All income and expenses are recognized only upon contract completion. Generally limited to small contractors meeting the IRS gross receipts threshold (currently $31 million average annual receipts under the small contractor exception) and to short-duration contracts. Provides tax deferral benefits but obscures real-time profitability. Used appropriately, CCM is GAAP-compliant for qualifying small contractors — not 'non-GAAP' as sometimes described.

CCA PRO TIP: For most small and mid-size California contractors, the cost-to-cost percentage-of-completion method is the right answer under ASC 606. CCM has a place for very small contractors with short-duration jobs, but it complicates surety underwriting and lender reporting. Discuss the method election with your CPA before defaulting to either. |

Not Sure If Your Books Are ASC 606 Compliant?

Most construction firms aren't — until their CPA flags it at year-end or a surety review catches it. CCA structures construction bookkeeping around ASC 606 from day one: proper performance obligations, correct percentage-of-completion calculations, and over/under billing tracked monthly. In a 30-minute call, we'll review your current accounting setup and tell you honestly whether it would survive a financial review.

Call or Text: (949) 889-3283

Cash vs Accrual Accounting

Beyond revenue recognition method, contractors also choose between two accounting bases:

Cash Basis

Revenue is recognized when cash is received; expenses when cash is paid. Accounts receivable and accounts payable do not appear on the financial statements. Provides clear visibility into actual cash flow but distorts profitability — a contractor can show "profit" in a month they collected on jobs completed six months earlier. Typically used by smaller contractors under the IRS gross receipts threshold.

Accrual Basis

Revenue is recognized when earned (billed); expenses when incurred. Both AR and AP appear on the balance sheet. Provides accurate profitability matching but does not directly reflect cash position. Required for GAAP financial statements, expected by sureties and most lenders, and used by virtually all mid-size and larger construction firms.

⚠ WATCH OUT: Many small contractors operate cash-basis for tax purposes but need accrual-basis financials for surety and lender review. The cleanest setup runs accrual books year-round with a tax-basis adjustment at year-end — not switching back and forth. CCA configures this dual treatment for construction clients who need both views. |

Construction Billing Methods

Billing structures matter to accounting because they determine when revenue is recognized, when cash is collected, and how variable consideration is handled. The five common methods:

Lump Sum (Fixed Price) — one fixed price for the entire scope. Risk sits with the contractor — overruns reduce profit. Common on residential and well-defined commercial work.

Cost-Plus — owner pays actual costs plus a fee (fixed amount or percentage). Risk sits with the owner. Common on negotiated commercial and tenant-improvement work. Requires precise cost tracking.

Time and Materials (T&M) — hourly labor rates plus actual material costs. Common for service work, change orders, and emergency repairs. Profitability depends entirely on accurate time and material tracking.

Unit Price — work is divided into measurable units (square feet, linear feet, cubic yards) priced individually. Common on public works and infrastructure projects.

AIA Progress Billing (G702/G703) — standardized monthly billing process using AIA forms. Most common on commercial and government work. The G703 schedule of values defines the line items, percent complete updates monthly, and the G702 application aggregates the billing. Requires architect approval before payment release.

Each method produces different cash flow patterns, different risk exposure, and different construction revenue recognition complexity. Many firms run different billing approaches across different customer segments — fixed-price for residential, AIA progress for commercial, T&M for service. The chart of accounts and project setup have to support all of them simultaneously.

Construction Retainage in 2026

Retainage is the portion of each progress payment withheld by the customer (or by the GC, on subcontractor invoices) until substantial completion or final acceptance. Standard rates in 2026 range from 5% to 10% of each payment, though some public works contracts in California allow lower retention after reaching 50% completion. Retainage is earned revenue you cannot collect — sometimes for months or years after the work is performed.

How Retainage Should Be Tracked

Proper retainage handling under construction accounting requires separating retention from regular AR:

Retention Receivable — tracked as a separate AR subaccount, distinct from current invoices. Aged differently. Reviewed monthly for release triggers.

Retention Payable — when you are holding retention from subs, this is a separate AP liability. Released according to the same terms in your sub agreements.

Release Triggers — substantial completion, final inspection, owner sign-off, lien-free certification. Each trigger should be tracked actively, not passively waited for.

BOOKKEEPER'S NOTE: Retainage that nobody chases is retainage that does not get collected. CCA includes retention release tracking as part of monthly AR review for construction clients — every retention balance over 60 days past the release trigger gets flagged for follow-up. This is one of the simplest cash flow improvements available to most contractors. |

The Modern Construction Accounting Software Stack

Software is one area where contractors most consistently over- or under-invest. A $3M residential remodeler paying for Sage 300 Construction is wasting money on features they will never use. A $30M commercial GC running QuickBooks Online is missing functionality they actually need. The right accounting for construction companies stack varies by firm size:

THE MODERN CONSTRUCTION ACCOUNTING SOFTWARE STACK

How software needs scale with firm size — and where contractors typically over- or under-invest

Small | $1M – $5M revenue | Accounting: QuickBooks Online + construction COA Project Mgmt: JobTread or Buildertrend Software Cost: ~$200 – $500/mo software Who Fits Here: Residential remodelers, custom builders, small specialty subs |

Mid | $5M – $25M revenue | Accounting: QuickBooks Enterprise OR Foundation Software Project Mgmt: Procore or Sage Intacct Construction Software Cost: ~$1,500 – $4,000/mo software Who Fits Here: Established GCs, mid-size commercial subs, multi-project firms |

Large | $25M+ revenue | Accounting: Sage 300 Construction, Viewpoint Vista, or CMiC Project Mgmt: Procore Enterprise or Trimble Construction One Software Cost: ~$5,000 – $20,000+/mo software Who Fits Here: Large GCs, ENR Top 400, multi-state contractors |

Source: Construction Cost Accounting | constructioncostaccounting.com

Where Most Contractors Should Land

The honest answer for most Orange County contractors in the $1M–$15M range: a properly configured QuickBooks Online setup (or QuickBooks Enterprise as you scale) paired with JobTread or Procore for project management is sufficient. The bottleneck is not the software — it is the chart of accounts structure, the job costing discipline, and the monthly close process. Spending more on software does not fix any of those. CCA configures and maintains QuickBooks for construction firms in this revenue range every month.

Construction Accounting Principles: What Best-in-Class Firms Do

The construction firms that scale through 2026 without running into cash or compliance trouble share a set of construction accounting practices that distinguish them from firms that grow into difficulty. The seven we see consistently:

1. Project-level accounting from day one — every dollar of revenue and cost ties to a specific job. No floating expenses that cannot be allocated. No 'overhead' items hiding direct project costs.

2. Monthly close by the 10th — not quarterly, not at year-end. The earlier each month is closed, the faster cost overruns and billing errors get caught.

3. Monthly WIP reports — every active job's status reviewed monthly: contract value, costs to date, percent complete, billed to date, over/under billing. Surety and CPA both expect this.

4. ASC 606 compliance baked in — performance obligations identified at contract signing, variable consideration constrained appropriately, revenue recognition documented monthly.

5. Active receivables management — aging review, retention tracking, proactive collection follow-up. Most contractors leave money on the table here.

6. Real-time job costing — Procore or JobTread synced to QuickBooks so PMs see live cost data and overruns get flagged immediately.

7. Year-end ready by November — CPA-ready financials and WIP schedules prepared two months before they are due. No scrambling in March.

Best-in-class contractors do not have better instincts than their peers. They have better systems. Disciplined construction accounting is the system that makes everything else possible. |

Where Construction Cost Accounting Fits In

Construction Cost Accounting is a construction bookkeeping services firm and QuickBooks ProAdvisor practice built specifically for contractors in Orange County and across California. Our work is the monthly operating system that makes everything in this guide actually happen:

Construction-specific chart of accounts — built or rebuilt for each new client so job costing and overhead allocation work properly.

Monthly close by the 10th — P&L, balance sheet, AR aging, AP aging, retention tracking — closed and delivered the same week every month.

WIP reporting by job — every active project's status: percent complete, earned revenue, billed to date, over/under billing — in the format your CPA and surety expect.

ASC 606 revenue recognition — monthly review of variable consideration, performance obligations, and revenue recognition across all active contracts.

Job costing integration — Procore, JobTread, or other project management software synced cleanly to QuickBooks so PMs and accounting see the same numbers.

Retention and lien tracking — retention receivable aged and chased, retention payable tracked against sub agreements, release triggers monitored.

Year-end financial statements — CPA-ready financials and WIP schedules in the format your surety and lender expect.

As a marketing agency for construction financial clarity — and an SEO marketing agency focused on Orange County contractors — CCA's role is to make the difference between knowing what your books say and acting on what they say. The construction bookkeeper who closes your month is the one who tells you which jobs to take on next, which customers to extend credit to, and which projects need a hard conversation before next quarter.

In 2026, construction accounting is the discipline that separates contractors who scale sustainably from those who grow into bankruptcy. The math is straightforward: a properly built construction chart of accounts, ASC 606-compliant revenue recognition, monthly close by the 10th, WIP reports by job, and active retention tracking — these are not optional or advanced techniques. They are the standard for any accounting for contractors operation that intends to survive the next decade.

If your firm is not running monthly job costing, monthly WIP reporting, and an ASC 606-aware close process, the books you are operating from are not telling you the truth about your business. Construction Cost Accounting handles all of it as part of standard construction bookkeeping services — proper chart of accounts, monthly close by the 10th, WIP reporting, ASC 606 revenue recognition, and CPA-ready financials. Most contractors who switch to us see their first complete monthly close within 30 days of onboarding.

Want to go deeper on the financial side? Our 2026 guide to construction working capital benchmarks. Want to see how project management software ties into accounting? Start with JobTread or Procore's QuickBooks integration.

Stop Treating Construction Accounting Like Regular Accounting

Construction accounting requires job-by-job tracking, ASC 606 revenue recognition, retainage management, and WIP reporting most regular bookkeepers have never seen. Every month CCA delivers: monthly close by the 10th, job costing by project, WIP report, retainage tracking, and the financial reports your surety and CPA expect. Built for contractors. Run by a QuickBooks ProAdvisor.

Call or Text: (949) 889-3283

Sources & Further Reading

Construction Financial Management Association (CFMA) — industry standards and benchmarking (cfma.org)

FASB ASC 606 Revenue from Contracts with Customers — official standard (fasb.org)

AICPA Audit and Accounting Guide: Construction Contractors — industry-specific audit and accounting guidance (aicpa.org)

Comments